Watching a water stain grow on your ceiling during an Arizona monsoon is a special kind of dread. Your mind immediately jumps to repair costs, followed by the big question: "Is a roof leak covered by insurance?" The answer is often yes, but it hinges on one critical factor: the cause. If the leak is from a sudden, accidental event like a storm, you're likely in good shape. But if it's due to old age or lack of maintenance, you'll probably have to cover the cost yourself.

Navigating the world of insurance claims can feel overwhelming, especially when you're already stressed about water damage. This guide is designed to be your roadmap, breaking down the complexities of your policy, explaining what is and isn't covered, and providing a clear, step-by-step plan for filing a successful claim.

Key Takeaways

- Cause is Everything: Coverage almost always comes down to why your roof is leaking. If a specific event like a windstorm, a hail storm, or a fallen tree is the culprit, you're generally in good shape.

- Maintenance Matters: The most common reason for a denied claim? Gradual wear and tear, old age, or putting off necessary repairs. Insurance companies expect you to keep up with routine maintenance.

- Documentation is Your Power: You have to prove your case. Take plenty of photos and videos of the damage, both inside your home and on the roof itself. This evidence is your best friend when the adjuster shows up.

- Act Quickly: Don't wait. Report the leak to your insurance provider as soon as you discover it. If you delay, they might argue that you let the damage get worse, which could jeopardize your claim.

Decoding Your Homeowners Insurance Policy

Let's be honest, trying to read an insurance policy can feel like wading through legal jargon. It's dense, confusing, and seems designed to be anything but clear. But when your roof is leaking, you need to know exactly where you stand. So, let’s cut through the noise and figure out what your policy actually says about roof damage.

Think of your policy as the rulebook for a game. To win the "get your roof paid for" game, you need to know which events, or "perils," are in play.

Named Perils vs. Open Perils

Your policy's structure is the first thing to understand, and it usually falls into one of two camps. The difference between them is huge.

- Named Perils Policy: This is like a very specific checklist. Your roof damage is covered only if the cause is one of the events explicitly listed in the policy—things like fire, hail, or a windstorm. If the cause isn't on that specific list, you're on your own.

- Open Perils Policy (or All-Risk): This works the opposite way. It covers damage from any cause, unless it’s specifically listed in the exclusions section. This gives you much broader protection, but you still have to watch out for the fine print, which almost always excludes things like basic wear and tear.

No matter which type of policy you have, insurance companies live by one golden rule: the damage must be sudden and accidental. This is the lens through which every adjuster will view your claim.

A classic Arizona example? A fierce monsoon storm rolls in, and a microburst peels a section of your shingles back like a can opener. The resulting leak is a textbook case of sudden and accidental damage. On the flip side, a slow drip from a leak that’s been developing for months because your 20-year-old shingles are brittle and cracked won’t be covered. That's considered gradual damage from a lack of maintenance.

The key distinction for an insurer is whether the damage was an unforeseeable event or the result of predictable aging and lack of maintenance.

Understanding Your Financial Payout

Okay, so your claim is approved. The next big question is: how much money will you actually get? Three terms in your policy will determine the size of that check.

1. Your Deductible

This is your share of the cost. It’s the amount you have to pay out of your own pocket before the insurance company pays a dime. If your roof repair is $10,000 and you have a $2,000 deductible, your insurer will pay up to $8,000.

2. Actual Cash Value (ACV)

ACV pays you for what your old, damaged roof was worth at the moment it was damaged. It’s the replacement cost minus depreciation—the value it lost over the years from age and exposure to the elements. For an older roof, an ACV payout can be disappointingly small and won’t come close to covering the cost of a brand-new one.

3. Replacement Cost Value (RCV)

This is the coverage you want to have. RCV pays the full cost to replace your damaged roof with a new one of similar quality, without any deduction for depreciation. It’s designed to make you whole again, ensuring you have the funds to get the job done right.

Understanding this stuff is more important than ever. Severe weather is on the rise, and wind and hail damage now account for nearly 50% of all U.S. homeowners insurance claims. From 2018 to 2022, these storms were responsible for a staggering 42% of insured home losses. You can see more on these trends in this breakdown of roofing industry costs and damage on sunsent.com. Knowing your policy inside and out is the best way to prepare for whatever the weather throws your way.

What Types of Roof Damage Are Usually Covered?

When you discover a leak, the first question that pops into your head is always the same: is my roof leak covered by insurance? The answer really boils down to one simple thing: what caused the damage? Insurance companies draw a very clear line in the sand between sudden, accidental events and problems that crop up over time due to neglect.

Let's walk through the specific situations that typically get a green light from your insurance provider, especially considering the unique weather challenges we face here in Arizona.

Think of your policy less like a home warranty and more like a financial safety net for the truly unexpected. It’s designed to protect you from "perils"—unforeseeable incidents that cause damage out of the blue.

Damage from Wind and Monsoon Storms

Anyone who’s lived through an Arizona monsoon knows how violent they can be. Those sudden, high-powered winds from a microburst can easily get under your shingles, bending them back or ripping them right off the roof. Once that watertight seal is broken, you've got a problem. This is a textbook example of a covered event.

When an insurance adjuster comes out to look for wind damage, they’re hunting for specific clues:

- Missing Shingles: Obvious gaps where shingles used to be, leaving the underlayment exposed.

- Creased Shingles: A distinct horizontal line across a shingle where the wind folded it back on itself. This crease is permanent damage.

- Lifted Shingles: The adhesive strip that holds the shingle flat has been broken by the wind, making it easy for rain to get underneath.

Because this kind of damage is clearly tied to a specific storm, it's one of the most straightforward and commonly approved types of roof leak claims.

The Hidden Threat of Hail Damage

Hail is one of the trickiest—and most destructive—things your roof will ever face. Of course, golf-ball-sized hail will cause obvious damage, but even small, pea-sized hail can create tiny fractures that turn into major leaks weeks or even months down the road.

Insurance adjusters are trained to spot the tell-tale signs of hail impacts.

- Bruising and Fracturing: Hail can leave soft, spongy "bruises" on asphalt shingles where it has crushed the material and fractured the matting underneath. You often can't see this from the ground.

- Granule Loss: The impact knocks off the protective ceramic granules, exposing the raw asphalt to the sun's UV rays, which causes it to break down much faster.

- Dents and Cracks: On tile or metal roofs, hail leaves behind obvious cracks and dents that ruin the roof’s ability to properly shed water.

Because hail damage can be so subtle, it’s a good idea to get a professional inspection after any big hailstorm, even if you don't see a leak right away.

An adjuster will look for a consistent pattern of impacts across the entire roof to confirm the damage was from hail and not something else. A good roofer knows exactly how to document this evidence to build a rock-solid case for your claim. To get a better handle on this, check out our guide on navigating a storm damage roof insurance claim.

Other Common Covered Events

While wind and hail are the biggest culprits here in Arizona, your policy covers other sudden and accidental events that can lead to a leaky roof.

- Falling Objects: If a storm brings down a tree branch—from your yard or the neighbor's—and it smashes into your roof, the damage is almost always covered. This also applies to other debris tossed around by high winds.

- Lightning Strikes: A direct lightning strike can blast a hole right through your roof, start a fire, or send a shockwave that cracks tiles. Any leaks that result from this are a classic covered peril.

- Weight of Snow or Ice: For those in Northern Arizona, like Flagstaff, the sheer weight of heavy snow can cause structural damage. It can also lead to ice dams, where ice builds up at the edge of the roof and prevents melting snow from draining, forcing water back up under your shingles. This is also a standard covered event.

In all of these cases, the secret to a successful claim is proving the leak is a direct result of a single, sudden event. The evidence has to scream "accident," not "old roof." By understanding what adjusters are looking for, you can gather the right proof and give your claim the best possible chance of success.

Common Reasons a Roof Leak Claim Is Denied

It's just as important to understand why a claim gets denied as it is to know what gets approved. Nothing is more frustrating than dealing with a leak only to get a rejection letter from your insurance company. But most of the time, these denials aren't random—they're based on specific policy exclusions every property owner should be aware of.

By far, the most common reason for a denied claim is neglect or lack of maintenance. Insurance is there to protect you from sudden, accidental events, not the slow, predictable breakdown of a roof that hasn't been looked after.

Think of it like car insurance. It’ll cover a surprise fender-bender, but it won’t buy you new tires just because your old ones wore out after years on the road. An old, failing roof is seen in exactly the same light.

From the insurer's perspective, their job is to shield you from unexpected disasters, not to pay for a new roof that was needed because of old age or deferred maintenance.

Wear and Tear: The Silent Claim Killer

"Wear and tear" is the phrase you'll often hear from an insurance adjuster when a claim for an older roof is denied. Every roof, especially under the intense Arizona sun, eventually breaks down from heat, temperature swings, and seasonal storms.

Over time, shingles get brittle and crack. The flashing around pipes and vents can warp. Sealants dry out and fail. These are all expected parts of a roof's natural lifecycle. When a leak starts because of these age-related problems, it's considered a maintenance issue, not an insurable event. If an adjuster sees that your roof was already in bad shape before a storm, they'll likely argue the storm wasn't the real cause of the leak, and the claim will be quickly denied.

Faulty Workmanship and Installation Errors

Another major reason for denial is damage caused by improper installation. Let's say the contractor who put your roof on 5 years ago used the wrong fasteners or didn't seal the flashing correctly. A small leak might have been happening for years, only becoming obvious after a major downpour.

In that situation, the real problem isn't the storm—it's the shoddy workmanship. Your insurance policy is not a warranty for another contractor's mistakes. The only way to get it fixed would be to go after the original roofer's workmanship warranty, which can be a tough battle, especially if that company has since closed its doors.

Other Common Claim Denial Reasons

Beyond old age and bad installations, a few other things can get your claim tossed out. Knowing what they are ahead of time helps you manage expectations and focus on what you can actually control.

- Pest and Animal Damage: If squirrels chew through your shingles or termites damage the decking, the resulting leak typically isn't covered. Damage from living things is almost always excluded from standard policies.

- Settling or Foundation Issues: A house can shift on its foundation over time, which puts stress on the entire structure, including the roof. If this movement causes a crack or a leak, it's usually excluded under "earth movement" or "settling" clauses.

- Specific "Peril" Exclusions: While most policies cover wind and hail, they often leave out damage from floods, earthquakes, or mudslides. You'd need to buy separate, specialized coverage for those types of events.

Understanding these common pitfalls puts you in a much stronger position. It helps you shift your focus from simply hoping for coverage to actively preventing the kinds of problems that lead to denials. Regular inspections and being proactive with maintenance are your best defense, ensuring that when a real disaster does hit, your roof stands the best chance of a successful insurance claim.

How to File a Successful Roof Leak Insurance Claim

Discovering a leak is stressful enough without having to worry about the insurance claim. The first few steps you take can honestly make or break your entire claim, so knowing what to do is critical.

Let's walk through a clear, step-by-step playbook that turns a confusing mess into a manageable process.

Your First Moves: Damage Control

The moment you spot a water stain or hear that dreaded drip…drip…drip, your first job is to stop the problem from spiraling out of control. Insurance policies actually require you to take reasonable steps to mitigate further damage. This doesn’t mean you need to get on a slippery roof in the middle of a monsoon—it just means taking sensible, immediate action inside.

- Get furniture, electronics, and any other valuables out from under the leak.

- Put down buckets or pans to catch the water.

- If you can do it safely, tossing a tarp over the damaged spot on your roof can be a huge help in preventing more water from pouring in.

If you don't take these basic steps, your insurer could argue that your own inaction made the damage worse, and they might try to reduce your payout because of it.

Document Everything Meticulously

Your smartphone is your best friend right now. Before you touch a thing, start documenting. You need to think like a detective building a case—create a powerful visual record that leaves no room for questions.

Take plenty of clear photos and videos of everything you can:

- The water stains spreading across your ceiling or down the walls.

- The buckets actively catching water.

- Any damaged furniture, flooring, or personal belongings.

- If it’s safe, get pictures of the roof itself—show the missing shingles, hail dents, or the tree branch that caused the problem.

A detailed photographic timeline is your best evidence. It proves the damage happened as a direct result of a specific event and shows you acted quickly to prevent it from worsening.

Once you have this initial evidence locked down, it’s time to call your insurance agent or their claims hotline to officially report the damage. Have your policy number ready and be prepared to give a clear, simple rundown of what happened and when.

Prepare for the Adjuster and Inspection

After you file, the insurance company will send an adjuster to inspect the damage. This meeting is a pivotal moment in your claim, and being prepared is non-negotiable. The adjuster's job is to figure out how bad the damage is and what caused it, which directly determines if your roof leak covered by insurance gets a green light.

This is the perfect time to bring in your own expert. Having a professional roofer like AZ Roof Co inspect the damage gives you an advocate in your corner. We can meet the adjuster on-site, point out damage they might otherwise miss, and give them a detailed report in the exact language they understand. Our guide on the roof insurance claim process goes even deeper into why this is so important.

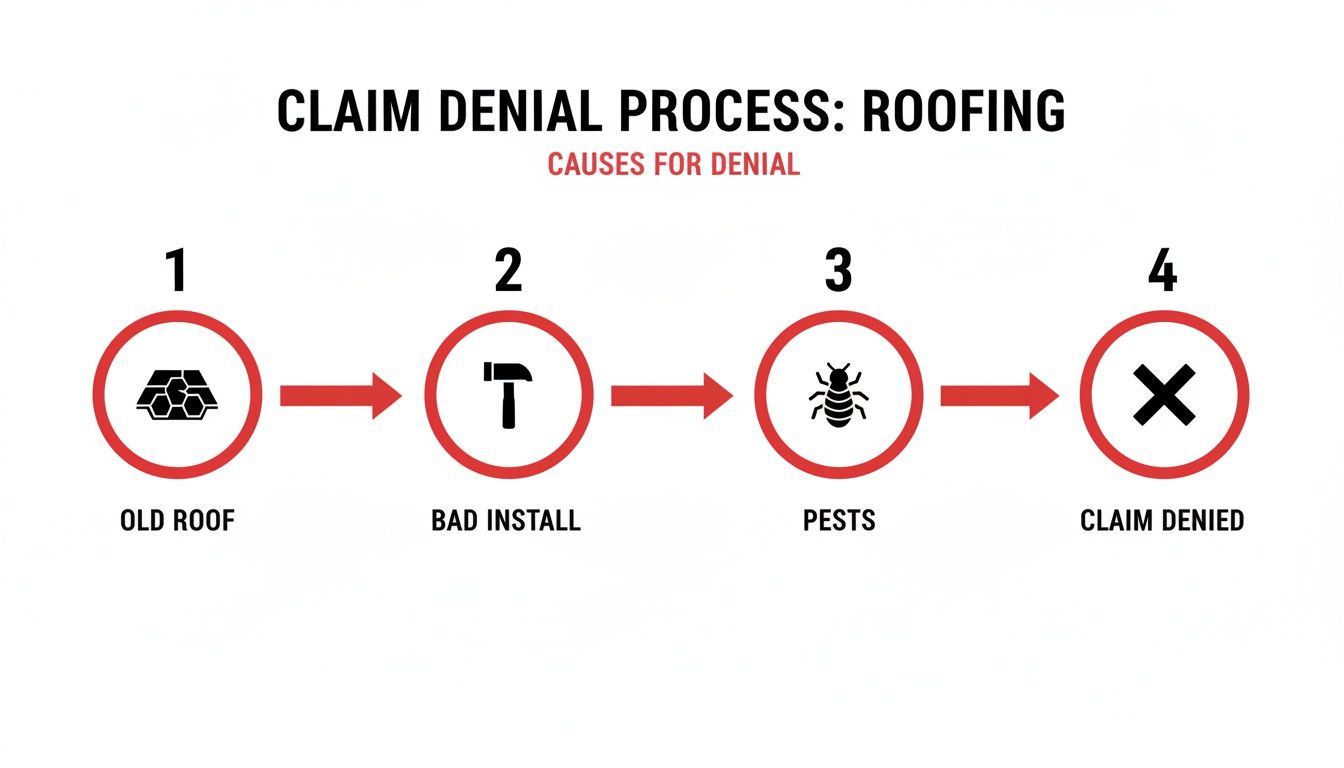

This flowchart shows some of the most common reasons an initial claim gets shot down, which really highlights why having professional backup is so valuable.

As you can see, things like old age, shoddy installation, or pest damage are frequent roadblocks—all of which are completely separate from the sudden, covered events you need to prove.

Understand Your Settlement Offer

If your claim is approved, you'll get a settlement offer. It’s important to know this usually comes in two parts, especially if your policy includes Replacement Cost Value (RCV).

- Initial Payment (Actual Cash Value): This is the first check you’ll receive. It covers what your damaged roof is worth today, factoring in depreciation for its age and condition, minus your deductible.

- Recoverable Depreciation: This is the second check, which covers the difference. You typically only get this money after the repairs are finished and you've sent the final contractor's invoice to the insurance company.

Read the adjuster’s report and the settlement offer very carefully. Make sure it accounts for all the damage, including the costs for materials, labor, and any city permits. If the offer seems too low or if the claim is denied outright, don't give up.

It’s crucial to understand how to appeal a denied insurance claim. With solid documentation and professional support, you can absolutely challenge an unfair decision and fight for the coverage you’ve been paying for.

How a Professional Roofer Can Maximize Your Claim

Trying to navigate a roof leak insurance claim by yourself can feel like an uphill battle. You're already stressed about the damage to your home, and now you have to decipher complex policy language. Bringing in an experienced roofer like AZ Roof Co completely changes the dynamic, turning a frustrating process into a manageable one.

Think of an expert roofer as your most valuable ally. We’re not just looking for a single leak; we're hunting down the source and documenting every bit of related damage to make sure your claim for a roof leak covered by insurance is as solid as it can possibly be.

The Power of a Professional Inspection

An insurance adjuster might only spend a few minutes on your roof, but a dedicated roofing professional conducts a much deeper dive. We know exactly what to look for—those subtle signs of storm damage that are easy to miss, like hidden hairline cracks in tiles or granule loss on shingles that point directly to a covered event like a hailstorm.

We use our experience and a deep understanding of Arizona's unique weather patterns to find the evidence that ties the damage directly to a specific storm. This detailed inspection becomes the bedrock of a successful claim. To see just how thorough we are, learn more about our professional roof inspection service.

This level of detail has never been more critical. Recently, U.S. roof repair and replacement claims have climbed to nearly $31 billion—a massive 30% increase from previous years. It's a clear sign that roofs are a major point of contention for both homeowners and insurers. You can find more details on these evolving roofing risks on Verisk.com.

Speaking the Adjuster’s Language

After our inspection, we put together a comprehensive report packed with photos. This is far more than a simple repair quote; it’s a detailed document written in the precise language adjusters expect and understand.

Your roofer’s report acts as a translator. It converts the physical damage into a clear, evidence-based story that lines up perfectly with what insurance companies need to see to approve a covered loss.

We meticulously document everything, including:

- The exact date and type of storm that caused the damage.

- Clear photographic evidence of every point of impact and failure.

- An itemized breakdown of all necessary repairs, from materials to labor costs.

- Citations of local building codes that might require certain upgrades during the repair.

We’ll even be there to meet the adjuster on-site for their inspection. By walking the roof with them, we can point out everything we found, answer their technical questions, and make sure nothing gets overlooked. This kind of partnership takes the pressure off you and dramatically increases the odds of getting a fair settlement that covers the full cost of restoring your home properly.

Frequently Asked Questions (FAQs)

How long do I have to file a roof leak claim?

Most insurance policies require you to file a claim within one to two years of the damage occurring. However, it's crucial to report the damage "promptly" or "as soon as reasonably possible." Waiting too long could give the insurer a reason to argue that you allowed the damage to worsen, potentially jeopardizing your claim. It's best to act within days or weeks of a major storm.

Will my insurance premiums go up if I file a roof leak claim?

Filing a single claim, especially after a widespread weather event that affected many homes in your area, does not automatically mean your rates will increase. Insurers typically raise rates for customers who file multiple claims in a short period. If the repair cost is only slightly more than your deductible, it may be wiser to pay out-of-pocket to avoid creating a claims history.

Does homeowners insurance cover the cost to repair the roof itself?

Yes, if the leak was caused by a covered peril (like wind, hail, or a fallen tree), your policy should cover the cost to repair the section of the roof that was damaged. In many cases, if a matching repair isn't possible, it may even cover the full replacement of that roof slope or the entire roof.

What if my claim is denied?

If your claim is denied, don't give up. First, ask your insurance company for a detailed written explanation for the denial, referencing the specific language in your policy. Then, gather all your documentation, including photos and a report from a trusted local roofer. You can appeal the decision with the insurer and, if that fails, consider hiring a public adjuster or consulting with an attorney who specializes in insurance claims.

Does insurance cover water damage from a roof leak?

Yes, in most cases, homeowners insurance will cover the interior damage caused by a roof leak (such as damaged ceilings, walls, and furniture), even if the cause of the roof leak itself (like old age) is not covered. This is known as "resultant damage" coverage. Always check your specific policy details to be sure.