A leaky, aging roof is more than just an eyesore; it's a major source of stress for any homeowner. The immediate concern is protecting your home and family, but the looming question is always, "How are we going to pay for this?" A full roof replacement is a significant investment, and the price tag can be daunting. For most people, paying out-of-pocket isn't realistic.

The good news is you have options. Understanding how to finance a roof replacement transforms the problem from an overwhelming expense into a manageable project. From tapping into your home's equity to securing a simple personal loan, a smart financing strategy can get you the high-quality, durable roof you need without draining your savings.

Key Takeaways

If you're just looking for the highlights, here’s what you absolutely need to know before you start the process of financing a new roof:

- Your main choices for funding are typically personal loans, home equity loans (or HELOCs), and direct financing through your roofing company. Each has its own pros and cons.

- Get at least three detailed quotes from trusted local roofers. You can't secure the right financing until you know exactly what you need to borrow.

- Check your homeowner's insurance policy first! If the damage is from a specific event, like a hailstorm or high winds, your insurance might cover a huge chunk of the cost.

Securing the right financing is just as important as choosing the right shingles. It ensures your project starts on solid financial ground, preventing future stress and protecting your investment in the long run.

Keep these points in mind as you move forward. In the sections ahead, we’ll dive deeper into each one, giving you the practical details needed to build a solid plan for getting your new roof.

Setting Your Budget Before Seeking Financing

Before you even think about how to pay for a new roof, you need to know what you’re up against financially. Applying for loans without a solid number in mind is a recipe for disaster. It can lead to borrowing too little and getting stuck mid-project, or borrowing too much and paying unnecessary interest.

The first move is always to get a handle on the real-world cost. That means calling in the pros.

Get Multiple, Detailed Quotes

Don't just get one estimate—aim for at least three from reputable, licensed roofing contractors in your area. A good quote is more than just a final price; it should give you a complete breakdown of where your money is going. Look for line items covering materials, labor, tear-off of the old roof, and any disposal fees.

This process isn't just about finding the cheapest option. It’s about understanding the true scope of the work and finding a contractor who is transparent and thorough.

Look Beyond the Shingles

One of the biggest mistakes I see homeowners make is budgeting only for what they can see. A new roof is much more than just shingles. What’s the condition of the plywood decking underneath? Is the flashing around your chimney and vents still solid? A proper inspection is non-negotiable, as it uncovers potential problems that can turn into massive, unexpected costs later.

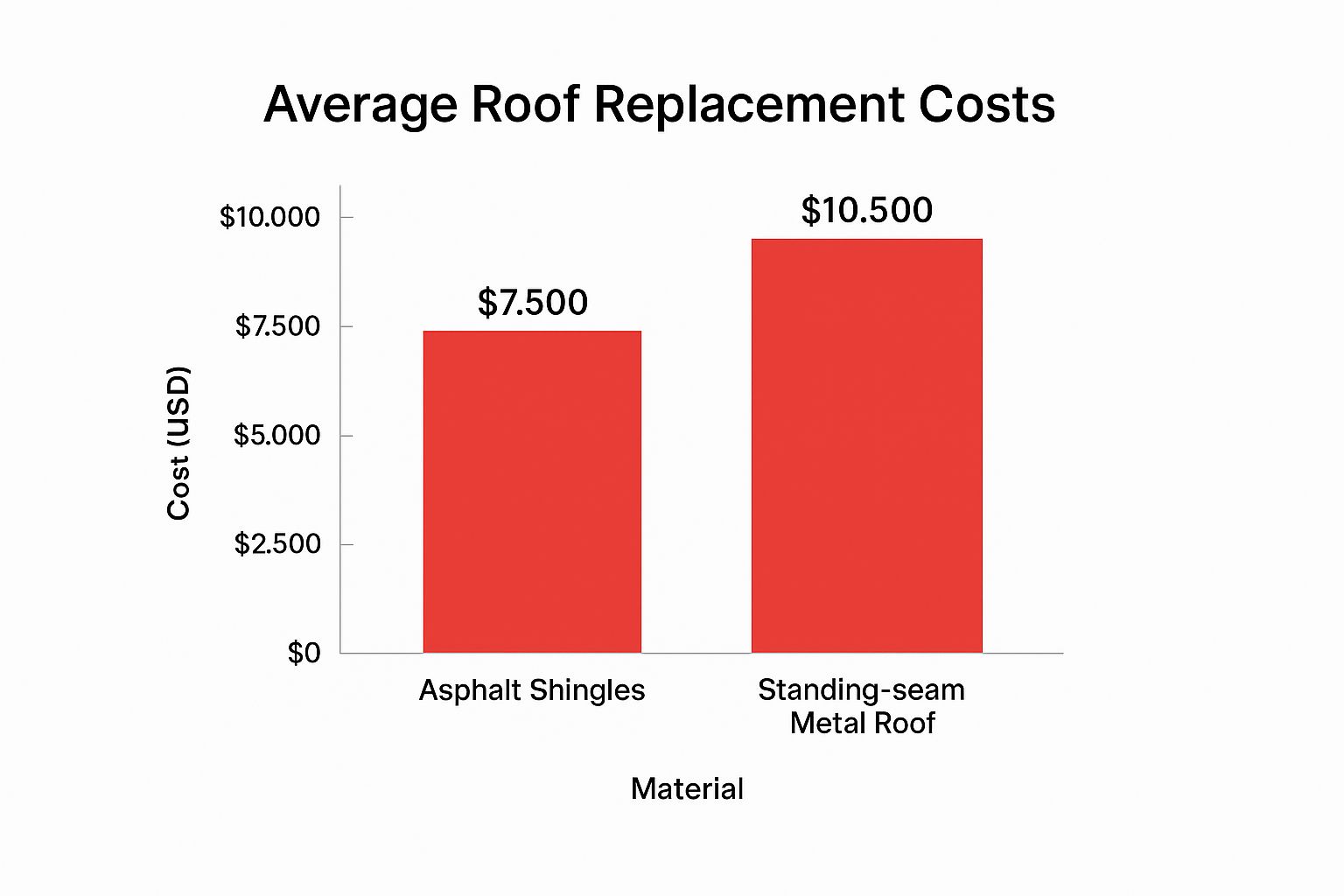

The materials you choose will also have a huge impact on your final budget. There’s a world of difference in cost between standard architectural shingles and a standing-seam metal roof.

This chart gives you a quick visual on how material choice can swing the total price.

As you can see, opting for a premium material like metal can easily double your project's cost compared to asphalt.

Nailing Down Your Final Number

Once you’ve gathered your quotes and settled on materials, it's time to put together your final project budget. This is the number you’ll take to lenders.

Nationally, roof replacements can run anywhere from $6,700 to a staggering $80,000, depending on the home’s size, complexity, and materials. To give you a ballpark:

- Asphalt shingles typically run $3 to $6 per square foot.

- Metal roofing can cost from $5 to $16 per square foot.

For a more tailored figure for your home, using a roof replacement cost estimator is a great way to get a more precise estimate.

Pro Tip: Your budget shouldn't stop at the contractor's quote. Always add a 10-15% contingency fund on top. This buffer is your safety net for any surprises, ensuring you have the financing to see the job through without the stress.

With this comprehensive number in hand, you're no longer guessing. You're ready to approach lenders with confidence, knowing exactly how much you need to secure.

Comparing Your Roof Financing Options

Once you've got a solid estimate in hand, the next big question is, "How am I going to pay for this?" This is where we dive into the world of roof financing. It's not a one-size-fits-all situation; the best path for you depends on your financial picture, your comfort with risk, and how quickly you need to get the project started.

Let's break down the most common ways homeowners fund a new roof, looking at everything from straightforward personal loans to using your home's equity.

Unsecured Personal Loans

Think of an unsecured personal loan as a direct, no-fuss way to get cash. You borrow a set amount from a bank, credit union, or an online lender and agree to pay it back in fixed monthly payments. The magic word here is unsecured—it means your house isn't on the line as collateral.

This makes the whole process pretty quick. In many cases, you can get approved and have the money in your account within a few business days. The trade-off? Because the lender is taking on more risk, the interest rates are generally higher than for loans secured by your home, especially if your credit score isn't top-tier.

- Who it’s for: Homeowners with solid credit who prioritize speed and don't want to tie the loan to their property.

- The upside: No risk to your home and a very fast funding timeline.

- The downside: You'll likely pay a higher interest rate than with other options.

Tapping Into Your Home's Equity

If you've been paying your mortgage for a while, you've likely built up some valuable home equity—that’s the difference between your home's market value and what you still owe. This equity can be a powerful tool for financing big projects. You generally have two ways to do it.

A home equity loan is pretty straightforward. You borrow a lump sum against your equity and pay it back with a fixed interest rate over a set term. It's predictable, which is perfect when you have a firm quote from your roofer and know the exact cost.

A Home Equity Line of Credit (HELOC) is more flexible, working a lot like a credit card. You get approved for a certain credit limit and can pull money out as you need it during a "draw period." This can be a lifesaver if unexpected repairs pop up mid-project, since you only pay interest on the amount you actually use.

The biggest draw for both of these options is the significantly lower interest rates. Because your home secures the loan, lenders see it as less risky. But that security comes with a serious condition: if you can't make the payments, you could risk foreclosure.

Financing Directly Through Your Roofer

Many reputable roofing companies, including us, have partnerships with lenders to offer financing directly to our customers. This is often the path of least resistance. You're handling the project and the payment plan all in one place, which cuts down on a lot of hassle.

The approval process is typically designed to be simple and fast. We often work with programs that offer flexible terms, like long-term payment plans or even promotional 0% interest periods. It's a fantastic way to get the work done now without the upfront financial hit. Just be sure to ask if the financing involves a lien on your property, as some programs work that way.

Roof Financing Options at a Glance

To make sense of it all, here is a comparison of common financing methods for a roof replacement. This table highlights key features to help you choose the best option for your financial situation.

| Financing Option | Best For | Typical Interest Rate | Key Benefit | Potential Drawback |

|---|---|---|---|---|

| Personal Loan | Homeowners with good credit who need funds quickly. | Moderate to High | Fast funding without using your home as collateral. | Can have higher interest rates than secured options. |

| Home Equity Loan | Homeowners with significant equity who prefer a fixed payment. | Low to Moderate | Lower, fixed interest rates and predictable payments. | Your home is collateral; the application can take longer. |

| HELOC | Projects with uncertain costs or those wanting flexibility. | Variable, often low | Draw funds as needed; only pay interest on what you use. | Rates can change over time; your home is collateral. |

| Contractor Financing | Those who value convenience and a streamlined process. | Varies (0% promos) | Simple, one-stop-shop experience with the roofer. | Terms can vary widely; may come with a lien. |

Ultimately, there's no single "best" choice—only the one that's right for you. It's about balancing interest rates, risk, and convenience to find the most comfortable and financially sound way to protect your home with a new roof.

Tapping Into Insurance and Government Programs

https://www.youtube.com/embed/K72Gty4KEMc

Before you even start looking at loans, it's smart to explore a few other avenues first. A lot of homeowners jump straight to thinking they have to foot the entire bill, but your insurance policy or even a government program could seriously lighten the financial load.

Figuring out how to use these resources can be the key to making your roof replacement affordable instead of a source of major financial stress.

Will Your Homeowners Insurance Cover a New Roof?

This is the big question, and the answer can be a bit tricky. Your homeowners insurance is there to protect you from sudden, unexpected damage—what the policy calls "perils." It’s not a maintenance plan for a roof that's just getting old.

So, when does insurance kick in? Typically, your policy will cover damage from things like:

- Weather Events: Think hailstorms, powerful wind, hurricanes, or tornadoes.

- Falling Objects: If a tree or a big branch comes down on your roof, that’s usually covered.

- Fire: Damage to your roof from a house fire is a classic example of a covered event.

The secret to a successful claim is proving the damage was caused by a specific event. This is where a good roofer is invaluable. They can inspect your roof and document whether the damage lines up with a recent storm, giving you the professional assessment you need to file your claim.

Finding Help with Government Assistance and Grants

Insurance isn't the only option out there. Several government-backed programs are designed to help homeowners with necessary repairs, especially for low-to-moderate-income families, seniors, veterans, or people in designated rural areas. You might be surprised at what's available.

For instance, the FHA Title I loan program is a popular choice for home improvements like roofing and often comes with more forgiving credit requirements. If you live in a rural area, the U.S. Department of Agriculture (USDA) has loans and grants specifically to help very-low-income homeowners make essential repairs.

Don't write yourself off. I’ve seen homeowners who were certain they wouldn't qualify discover they were eligible for thousands in assistance. An hour of research into local and federal programs is time well spent.

If you're dealing with unexpected financial strain, looking into hardship grants for individuals could also be a lifeline. We've also put together a detailed guide on how to get a new roof for free that dives deeper into these options.

With material costs on the rise, these programs are more critical than ever. The total cost for roof repairs and replacements in the U.S. shot up by nearly 30% between 2022 and 2024, hitting almost $31 billion. Much of that increase was fueled by storm damage. Tapping into these programs can make a huge difference in offsetting that financial pressure.

Alright, you've looked at the different ways to pay for your new roof and have a good idea of which path you want to take. Now comes the part that can feel a bit daunting: the loan application.

Honestly, it’s not as scary as it seems. The key is being prepared. If you have all your ducks in a row before you even start filling out forms, the whole thing goes much smoother, and you'll put yourself in the best position to get a great rate.

Start With Your Credit Score

Before a lender looks at anything else, they’re going to look at your credit score. It’s their first glimpse into your financial habits.

A strong credit score signals that you're a reliable borrower, which usually opens the door to better loan offers and, most importantly, lower interest rates. We're not talking about pocket change, either. A couple of percentage points can easily add up to thousands of dollars saved over the years you're paying back the loan.

So, the very first thing you should do is check your credit. You're entitled to a free report from each of the big three bureaus—Experian, Equifax, and TransUnion. Take a look. If your score is a little lower than you'd like, it might be worth taking a few months to pay down some credit card balances or dispute any errors you find. A little patience here can pay off big time.

Get Your Paperwork Ready

Lenders need to see proof that you can handle the loan, which means you’ll have to provide some documents. Getting these together now will save you a ton of back-and-forth later.

Think of it as your application toolkit. Here’s what you'll almost always need:

- Proof of Income: Typically your last two pay stubs. If you’re self-employed, have your most recent tax returns handy.

- Job Details: They'll want to verify your employment, so have your employer's contact info ready.

- Valid ID: A simple driver’s license or other government-issued photo ID will do the trick.

- The Contractor's Quote: This is a big one. The lender needs to see the official, itemized estimate from your roofer to justify the loan amount.

I always tell homeowners to scan these documents and save them in a folder on their computer. When you're applying online, you can just upload everything in a matter of minutes. It makes you look organized and serious, which never hurts.

How to Actually Compare Loan Offers

Getting approved is great, but don't just jump at the first offer you receive. You’ll likely get a few options, and picking the right one involves looking at more than just the interest rate.

When you're comparing loans, the most important number is the Annual Percentage Rate (APR). The APR includes the interest rate plus any fees the lender rolls into the loan. It gives you a much more accurate idea of what you'll actually be paying.

You also need to watch out for the fine print. Look for:

- Origination Fees: Some loans come with a processing fee, usually a percentage of the total loan amount.

- Loan Term: A longer repayment period means your monthly payment is lower, but you’ll pay much more in interest over the life of the loan.

- Prepayment Penalties: Some lenders will actually charge you a fee if you try to pay the loan off early. Make sure you can pay it down faster without a penalty.

Understanding the financing is just one part of a much bigger project. To see how this fits into the entire timeline, from tear-off to final inspection, take a look at our step-by-step guide to the roof replacement process. Taking the time to really examine each loan offer ensures you’re making a smart decision for your financial future, not just a quick fix for your roof.

Think Beyond the Repair: Turn Your New Roof Into a Smart Investment

You’ve navigated the financing maze and secured the funds for your new roof—that’s a huge win. But don't stop there. The smartest homeowners I work with don't just see this as a necessary repair; they see it as a strategic upgrade to one of their biggest assets.

Framing it this way changes everything. A high-quality roof is one of the most powerful tools you have for boosting your home's resale value and curb appeal. It’s often the first thing a potential buyer notices.

But the benefits don't stop at the curb. A new, properly installed roof can often lead to a pleasant surprise: lower homeowner's insurance premiums. From an insurer's perspective, a brand-new roof significantly reduces the risk of leaks, water damage, and storm-related claims, and they'll often reward you with a discount. It's always worth a call to your agent once the work is done.

Play the Long Game for the Best Return

This is where you can really make your money work for you. Choosing more durable, energy-efficient materials is the key to turning this expense into a true investment.

Yes, materials like metal or tile carry a higher price tag initially. But their incredible longevity and superior performance can save you a small fortune over the life of your home. Think fewer repairs and noticeably lower monthly energy bills, especially during those hot summer months.

The market is already heading in this direction. Industry forecasts show residential roofing spend is set to grow 8.2% annually, projected to hit $15 billion by 2025. What's driving this? Homeowners are increasingly opting for lifetime solutions like slate and tile, recognizing that the higher upfront cost is well worth the long-term payoff.

This is the mindset shift that makes all the difference. You're not just plugging a leak; you're investing in decades of energy savings, higher property value, and genuine peace of mind.

Finally, don't overlook the tax implications. Many homeowners tap into their home's equity to fund major projects like a roof replacement. If you do, it's absolutely essential to understand how maximizing mortgage interest deductions can further sweeten the deal. This is how you ensure your financing decision actively improves your home’s financial picture for years to come.

Frequently Asked Questions About Roof Financing

It’s completely normal to have questions when you're staring down a major expense like a new roof. It’s a big deal, and getting the financing right is just as important as choosing the right shingles. Let’s tackle some of the most common things homeowners ask so you can move forward with confidence.

Can I still finance a new roof if I have bad credit?

Yes, you absolutely can, but you'll need to be strategic. Having a lower credit score does narrow your options and often means facing higher interest rates, but it doesn't shut the door completely.

While a traditional bank might say no to an unsecured personal loan, don't stop there. Look into government-backed options like FHA Title I loans, which are specifically designed for home improvements and have more flexible credit requirements. Many roofing contractors also have their own financing partners who are used to working with a wider range of credit profiles.

A word of advice from experience: if you have a few months to spare, work on boosting your credit score first. Even a small jump can unlock much better loan terms. But if the roof can't wait, don't assume you're out of options.

Is putting a new roof on a credit card a good idea?

For the entire cost of a roof replacement, using a credit card is almost always a terrible idea. The interest rates are just too high. We're talking about standard APRs that can easily be double or triple what you’d get on a personal or home equity loan, which translates to thousands of extra dollars out of your pocket.

There is one exception, though. If you have a credit card with a 0% introductory APR and you are 100% certain you can pay off the entire balance before that intro period expires, it could work. But this is a risky play. For a project of this size, a structured loan is the safer, smarter financial path.

Will my homeowners insurance just pay for a new roof?

This is one of the biggest and most expensive misconceptions in roofing. The short answer is no, your insurance doesn't automatically cover a new roof just because it's old.

Homeowners insurance is there for sudden, accidental damage from a specific event, not for predictable aging and wear. Your policy will typically only kick in for damage caused by a "covered peril," like heavy winds from a documented storm, significant damage from a hailstorm, a house fire, or a tree falling on your house. If your roof is just reaching the end of its 20- or 30-year lifespan, the replacement cost is considered a homeowner's maintenance responsibility. Before you even think about filing a claim, get a professional roofer to perform a thorough inspection and document the exact cause of the damage. This documentation will be critical.